Amtrak's 2024 Ridership and Financials

Record ridership surpasses fiscal 2019 but the financial data is very concerning

My favorite early Christmas gift has come once again! With the release of Amtrak’s September 2024 Monthly Performance Report, their annual ridership, revenue, and expenses are available to the public for review. As anticipated from reports already put out by the state-supported services, passenger traffic has recovered to pre-Covid levels and surpassed 2019 to set a new record ridership in 2024. It has been a long journey from the depths of the pandemic era lockdowns and service suspensions, but in a brief four years Amtrak has recovered. It comes as a great relief to know that after it all, the passenger trains are still rolling.

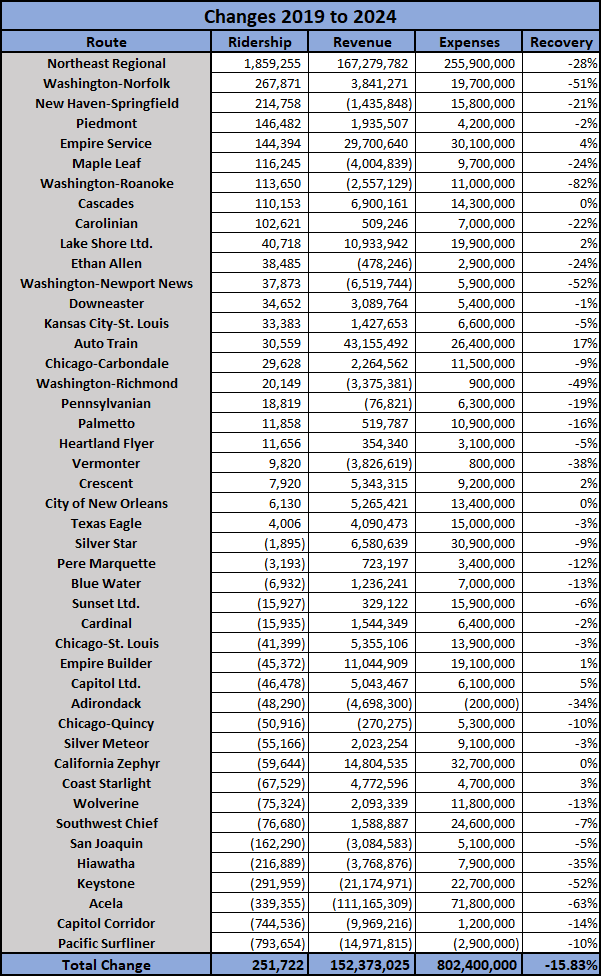

Every year I do a financial analysis with the goal of determining fare recovery.

% Fare Recovery = $ Operating Income / $ Operating Expenses.

In simple terms, does running a train generate a net profit or a net loss? All credit for this idea goes to Paul Druce, who began running these numbers in 2011 on his blog, which inspired me to keep doing so for my own benefit. I also repeat the analysis for Brightline, Caltrain, and Via Rail Canada to provide a full picture of what I would consider intercity trains in North America. None of those agencies have issued final reports for the year so for now it’s just Amtrak. With no further ado, sorted by 2024 ridership…

Green = National Network, White = State Supported, Blue = Northeast Corridor

I would like to take this moment to note that the revenue is ticket income only. Many breathless articles were issued in 2019 saying that Amtrak almost turned an operating profit, but this ignored the fact that the operating revenues included state funding, leaving only the National Network’s losses and the Northeast Corridor’s profits to be considered. I do not find this fair, the National Network receives operating subsidies from Washington, the corridor services receive it from the states, but a subsidy is a subsidy. Therefore, ticket revenue is the most objective standard to use for comparisons.

There is much to celebrate here, in particular the higher ridership which has resulted from running more trains on high demand corridors. Amtrak’s results so far present a stark contrast to the commuter railroads which have not seen ridership return to pre-Covid levels. What concerns me is that much of the increased ridership appears to be due to dropping ticket prices on routes with states willing to increase the rate of subsidy. Restoring ridership has come at a steep cost.

Take the worst offender, the Vermonter.

Despite increasing ridership by 9,820, revenue per passenger dropped $(41.26). Fare recovery declined from 63.80% to 26.09%. This is catastrophic for a route which was once one of the best financial performers of the state supported corridors.

The Virginia Services have gone from collectively profitable pre-Covid to losing an average of $(27.69) per passenger despite record ridership. Between the four routes, passenger volumes increased by 439,543, or 43.54%. This incredible increase in patronage in Virginia, which once led me to believe that Amtrak might be in a strong position headed into 2025, instead fills me now with deep concern. Sacrificing financially viable routes to drive ridership exposes Amtrak to the threat of severe service cuts and defunding by hostile political forces.

That is not a tolerable risk.

Other routes have been damaged by remote work; the most business class oriented trains such as the Hiawatha, Capitol Corridor, Pacific Surfliner, and the Acela all saw significant declines for a total of 2,094,434 fewer riders. The Acela alone represents a $(111,165,309) decline in revenue and the second worst drop in overall profitability across the entire network. For a train which made back 195.84% of its operating costs in 2019, this is a serious fall from grace that needs to be addressed immediately.

In sum total though, Amtrak’s overall challenge is not as much a lack of revenue as the rapidly increasing labor cost of passenger trains. Labor has always represented a disproportionate burden on operations for Amtrak and the commuter railroads. To wit in the words of somebody I unfortunately can’t remember, ‘people are the worst cargo’. It takes two employees to run a freight train, while passenger rail requires many more workers to maintain a level of service quality worth providing. Striking a balance between adequate service quality to attract riders and the financial realities of Amtrak surviving a potentially hostile administration in Washington will be very difficult moving forward.

All of this begs the question: What now?

Since Covid, Amtrak has successfully rebuilt its brand, begun investing billions of dollars into its infrastructure, set a new ridership record, begun running more frequent trains, and extended three routes. These are all achievements worth celebrating. At the same time, our national passenger rail service is too politically and financially vulnerable heading into a critical growth period. I will continue to watch future monthly reports with interest to see if the situation continues to trend towards even greater success. Until then, I will take the wins where we can get them and accept that some of this could not have been avoided. Covid may be gone, but it’s legacy is taking time to overcome.